Economics Problem Solving: Advantages, Definitions, and Monopoly Control

Okay, I will solve the questions one by one in a structured format.

Question 1

Describe five advantages of transition period in an economy.

The transition period in an economy refers to the shift from one economic system to another, often from a centrally planned economy to a market-based economy. Here are five advantages of such a transition:

- Increased Efficiency: Market-based economies allocate resources more efficiently through the price mechanism. This leads to better utilization of resources and higher productivity.

- Innovation and Entrepreneurship: The profit motive encourages innovation and entrepreneurship. New businesses and industries emerge, fostering economic growth and creating jobs.

- Greater Consumer Choice: Market economies offer a wider variety of goods and services, allowing consumers to satisfy their preferences more effectively.

- Improved Quality: Competition among firms leads to improved product quality and better customer service.

- Integration with the Global Economy: Transition economies can integrate more easily into the global economy, attracting foreign investment and benefiting from international trade.

Question 2

Define economics according to Lionel Robbins and provide its superiority over earlier definitions of economics. Give four points.

Lionel Robbins defined economics as:

"Economics is the science which studies human behavior as a relationship between ends and scarce means which have alternative uses."

Superiority over Earlier Definitions:

- Scarcity Focus: Robbins' definition emphasizes scarcity as a fundamental economic problem, which is a more realistic and universally applicable concept.

- Universality: It is not limited to material welfare but encompasses all human behavior involving choices under scarcity, making it more comprehensive.

- Analytical Precision: Robbins' definition provides a clearer and more precise framework for economic analysis.

- Scope: It broadens the scope of economics to include non-market activities and decision-making processes in various contexts.

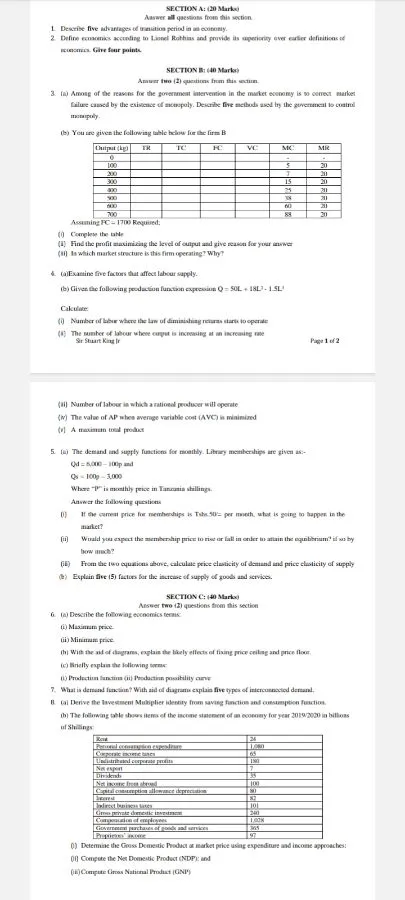

Question 3 (a)

Among of the reasons for the government intervention in the market economy is to correct market failure caused by the existence of monopoly. Describe five methods used try the government to control monopoly.

Government intervention is often necessary to mitigate the adverse effects of monopolies. Here are five methods governments use to control monopolies:

- Antitrust Laws: These laws prohibit anti-competitive behavior, such as price-fixing, market allocation, and predatory pricing. They promote competition by preventing the formation of monopolies and breaking up existing ones.

- Regulation: Governments can regulate the prices and output of monopolies to ensure fair pricing and adequate supply. This is common in industries like utilities (e.g., water, electricity).

- Nationalization: The government can take ownership of a monopoly, converting it into a public enterprise. This allows the government to control the industry directly and ensure that it operates in the public interest.

- Promoting Competition: Governments can encourage competition by reducing barriers to entry, such as licensing requirements and tariffs. This allows new firms to enter the market and challenge the dominance of the monopoly.

- Price Controls: Implementing price ceilings to prevent monopolies from charging excessively high prices.

Okay, let's continue with questions 4 to 8.

Question 4 (a)

Examine five factors that affect labor supply.

Five factors that affect labor supply are:

- Wage Rate: Higher wages generally incentivize more people to offer their labor.

- Population Size: A larger population typically means a larger potential labor force.

- Education and Skills: The availability of skilled workers affects the quality and quantity of labor supply.

- Government Policies: Policies such as minimum wage laws, unemployment benefits, and retirement age can influence labor supply.

- Cultural and Social Norms: Societal attitudes towards work, gender roles, and work-life balance can impact labor force participation rates.

Question 4 (b)

Given the following production function expression: \(Q = 50L + 18L^2 - 1.5L^3\)

Calculate:

(i) Number of labor where the law of diminishing returns starts to operate

The law of diminishing returns starts when the marginal product of labor (MPL) begins to decrease. To find this, we need to find the second derivative of the production function with respect to L and set it to zero.

First, find the first derivative (MPL):

\(MPL = \frac{dQ}{dL} = 50 + 36L - 4.5L^2\)

Next, find the second derivative:

\(\frac{d^2Q}{dL^2} = 36 - 9L\)

Set the second derivative to zero to find the inflection point:

\(36 - 9L = 0\)

\(9L = 36\)

\(L = 4\)

So, the law of diminishing returns starts to operate when \(L = 4\).

(ii) The number of labor where output is increasing at an increasing rate

Output increases at an increasing rate until the inflection point of the production function. This is the same point where the second derivative is zero, which we already found to be \(L = 4\).

(iii) Number of labor in which a rational producer will operate

A rational producer will operate where the MPL is positive but decreasing. This is after the law of diminishing returns has set in but before MPL becomes negative.

\(MPL = 50 + 36L - 4.5L^2 > 0\)

To find where MPL becomes negative, solve for \(L\):

\(50 + 36L - 4.5L^2 = 0\)

Using the quadratic formula:

\(L = \frac{-36 \pm \sqrt{36^2 - 4(-4.5)(50)}}{2(-4.5)}\)

\(L = \frac{-36 \pm \sqrt{1296 + 900}}{-9}\)

\(L = \frac{-36 \pm \sqrt{2196}}{-9}\)

\(L = \frac{-36 \pm 46.86}{-9}\)

We have two possible values for L:

\(L_1 = \frac{-36 + 46.86}{-9} \approx -1.21\) (which doesn't make sense in this context)

\(L_2 = \frac{-36 - 46.86}{-9} \approx 9.21\)

So, a rational producer will operate between \(L = 4\) and \(L \approx 9.21\).

(iv) The value of AP when average variable cost (AVC) is minimized

\(Q = 50L + 18L^2 - 1.5L^3\)

\(AP = \frac{Q}{L} = 50 + 18L - 1.5L^2\)

To find where AVC is minimized, we need to find where AP is maximized. Take the derivative of AP with respect to L and set it to zero:

\(\frac{dAP}{dL} = 18 - 3L = 0\)

\(3L = 18\)

\(L = 6\)

Now, find the value of AP when \(L = 6\):

\(AP = 50 + 18(6) - 1.5(6^2) = 50 + 108 - 54 = 104\)

(v) A maximum total product

Maximum total product occurs when MPL = 0:

\(50 + 36L - 4.5L^2 = 0\)

We already solved this in part (iii):

\(L \approx 9.21\)

Now, find the maximum total product by plugging this value of L into the production function:

\(Q = 50(9.21) + 18(9.21)^2 - 1.5(9.21)^3\)

\(Q \approx 50(9.21) + 18(84.82) - 1.5(780.59)\)

\(Q \approx 460.5 + 1526.76 - 1170.885\)

\(Q \approx 816.375\)

Question 5 (a)

The demand and supply functions for monthly library memberships are given as:

\(Q_d = 8,000 - 100P\) and \(Q_s = 100P - 3,000\)

Where "P" is the monthly price in Tanzania shillings.

(i) If the current price for memberships is Tshs 50 per month, what is going to happen in the market?

\(Q_d = 8,000 - 100(50) = 8,000 - 5,000 = 3,000\)

\(Q_s = 100(50) - 3,000 = 5,000 - 3,000 = 2,000\)

Since \(Q_d > Q_s\), there is a shortage in the market.

(ii) Would you expect the membership price to rise or fall in order to attain the equilibrium? If so by how much?

To find the equilibrium price, set \(Q_d = Q_s\):

\(8,000 - 100P = 100P - 3,000\)

\(11,000 = 200P\)

\(P = \frac{11,000}{200} = 55\)

The equilibrium price is 55 Tshs. Since the current price is 50 Tshs, the price is expected to rise by 5 Tshs to reach equilibrium.

(iii) From the two equations above, calculate price elasticity of demand and price elasticity of supply

Price elasticity of demand (PED) is calculated as:

\(PED = \frac{\% \Delta Q_d}{\% \Delta P} = \frac{P}{Q_d} \cdot \frac{dQ_d}{dP}\)

\(\frac{dQ_d}{dP} = -100\)

At \(P = 50\), \(Q_d = 3,000\)

\(PED = \frac{50}{3,000} \cdot (-100) = -\frac{5,000}{3,000} = -\frac{5}{3} \approx -1.67\)

Price elasticity of supply (PES) is calculated as:

\(PES = \frac{\% \Delta Q_s}{\% \Delta P} = \frac{P}{Q_s} \cdot \frac{dQ_s}{dP}\)

\(\frac{dQ_s}{dP} = 100\)

At \(P = 50\), \(Q_s = 2,000\)

\(PES = \frac{50}{2,000} \cdot (100) = \frac{5,000}{2,000} = \frac{5}{2} = 2.5\)

Question 5 (b)

Explain five (5) factors for the increase of supply of goods and services.

Five factors that can increase the supply of goods and services are:

- Technological Advancements: Improvements in technology can increase productivity and reduce production costs, leading to higher supply.

- Lower Input Costs: A decrease in the cost of raw materials, labor, or energy can make production more profitable, encouraging firms to supply more.

- Government Subsidies: Subsidies can lower the cost of production, incentivizing firms to increase supply.

- Increased Number of Sellers: More firms entering the market increase the overall supply of goods and services.

- Favorable Weather Conditions: In agriculture, good weather can lead to higher yields and increased supply.

Question 6 (a)

Describe the following economics terms:

(i) Maximum price

Maximum price, also known as a price ceiling, is a government-imposed limit on how high a price can be charged for a product. It is typically set below the equilibrium price to make goods more affordable for consumers.

(ii) Minimum price

Minimum price, also known as a price floor, is a government-imposed limit on how low a price can be charged for a product. It is typically set above the equilibrium price to protect producers by ensuring they receive at least a certain amount for their goods or services.

Question 6 (b)

With the aid of diagrams, explain the likely effects of fixing price ceiling and price floor.

Price Ceiling:

- When a price ceiling is set below the equilibrium price, it creates a shortage because the quantity demanded exceeds the quantity supplied.

- Diagram: A supply and demand graph showing the equilibrium price and quantity. A horizontal line below the equilibrium price represents the price ceiling. The quantity demanded at the ceiling price is greater than the quantity supplied, illustrating the shortage.

Price Floor:

- When a price floor is set above the equilibrium price, it creates a surplus because the quantity supplied exceeds the quantity demanded.

- Diagram: A supply and demand graph showing the equilibrium price and quantity. A horizontal line above the equilibrium price represents the price floor. The quantity supplied at the floor price is greater than the quantity demanded, illustrating the surplus.

Question 6 (c)

Briefly explain the following terms:

(i) Production function

Production function is an equation or mathematical expression that shows the relationship between the quantity of inputs (such as labor, capital, and raw materials) a firm uses and the quantity of output it produces. It represents the maximum amount of output that can be produced from a given set of inputs, assuming efficient production methods.

(ii) Production possibility curve

Production possibility curve (PPC), also known as a production possibility frontier (PPF), is a graphical representation showing the maximum combinations of two goods or services that an economy can produce when all resources are fully and efficiently utilized. It illustrates the concepts of scarcity, trade-offs, and opportunity cost.

Question 7

What is demand function? With aid of diagrams explain five types of interconnected demand.

Demand function is a mathematical relationship showing how the quantity demanded of a good or service depends on its price and other factors such as income, prices of related goods, and consumer tastes.

Five types of interconnected demand:

- Direct Demand: The demand for a good or service that satisfies a consumer's wants directly.

- Diagram: A typical demand curve showing the inverse relationship between price and quantity demanded.

- Derived Demand: The demand for a good or service that is used as an input in the production of another good or service.

- Diagram: An example could be the demand for steel derived from the demand for cars. As the demand for cars increases, the demand for steel also increases.

- Joint Demand: The demand for two or more goods that are used together.

- Diagram: An example is the demand for printers and ink cartridges. An increase in the demand for printers leads to an increase in the demand for ink cartridges.

- Composite Demand: The demand for a good that can be used for multiple purposes.

- Diagram: An example is the demand for steel, which can be used in construction, manufacturing, and transportation.

- Competitive Demand: The demand for goods that are substitutes for each other.

- Diagram: An example is the demand for Coke and Pepsi. An increase in the price of Coke may lead to an increase in the demand for Pepsi.

Question 8 (a)

Derive the Investment Multiplier identity from saving function and consumption functions.

Let's define the following:

* \(Y\) = Income

* \(C\) = Consumption

* \(S\) = Savings

* \(I\) = Investment

We know that:

\(Y = C + S\) (Income is either consumed or saved)

\(Y = C + I\) (In equilibrium, income equals consumption plus investment)

From these, we can say:

\(C + S = C + I\)

\(S = I\) (Savings equals investment in equilibrium)

Let's define the consumption function as:

\(C = a + bY\)

Where:

* \(a\) = Autonomous consumption (consumption independent of income)

* \(b\) = Marginal propensity to consume (MPC)

The saving function is:

\(S = Y - C\)

\(S = Y - (a + bY)\)

\(S = -a + (1 - b)Y\)

Where:

* \((1 - b)\) = Marginal propensity to save (MPS)

Now, let's derive the investment multiplier. Suppose investment increases by \(\Delta I\). This leads to an increase in income \(\Delta Y\).

\(\Delta Y = \Delta C + \Delta I\)

\(\Delta C = b \Delta Y\) (Change in consumption is MPC times the change in income)

Substitute \(\Delta C\) into the equation:

\(\Delta Y = b \Delta Y + \Delta I\)

\(\Delta Y - b \Delta Y = \Delta I\)

\(\Delta Y (1 - b) = \Delta I\)

\(\Delta Y = \frac{\Delta I}{1 - b}\)

The investment multiplier (k) is the ratio of the change in income to the change in investment:

\(k = \frac{\Delta Y}{\Delta I} = \frac{1}{1 - b}\)

Since \((1 - b)\) is the marginal propensity to save (MPS), we can also write:

\(k = \frac{1}{MPS}\)

Thus, the investment multiplier identity is derived from the saving and consumption functions and is equal to \(\frac{1}{1 - MPC}\) or \(\frac{1}{MPS}\).

Question 8 (b)

The following table shows items of the income statement of an economy for the year 2019/2020 in billions of Shillings:

| Item | Amount |

|---|---|

| Rent | 24 |

| Personal consumption expenditure | 1,080 |

| Corporate income taxes | 65 |

| Undistributed corporate profits | 150 |

| Net export | 7 |

| Dividends | 35 |

| Net income from abroad | 100 |

| Capital consumption allowance depreciation | 80 |

| Interest | 82 |

| Indirect business taxes | 101 |

| Gross private domestic investment | 240 |

| Compensation of employees | 1,078 |

| Government purchases of goods and services | 365 |

| Proprietors' income | 97 |

(i) Determine the Gross Domestic Product at market price using expenditure and income approaches:

Expenditure Approach:

GDP = Personal consumption expenditure + Gross private domestic investment + Government purchases of goods and services + Net export

GDP = 1,080 + 240 + 365 + 7 = 1,692 billions of Shillings

Income Approach:

GDP = Compensation of employees + Proprietors' income + Rent + Interest + Corporate profits + Indirect business taxes + Depreciation

Corporate profits = Corporate income taxes + Undistributed corporate profits + Dividends

Corporate profits = 65 + 150 + 35 = 250

GDP = 1,078 + 97 + 24 + 82 + 250 + 101 + 80 = 1,712 billions of Shillings

(ii) Compute the Net Domestic Product (NDP):

NDP = GDP - Depreciation

Using the GDP from the income approach:

NDP = 1,712 - 80 = 1,632 billions of Shillings

(iii) Compute Gross National Product (GNP):

GNP = GDP + Net income from abroad

Using the GDP from the income approach:

GNP = 1,712 + 100 = 1,812 billions of Shillings